》Check SMM copper quotes, data, and market analysis

》Subscribe to view historical spot prices of SMM metals

》Click to view the SMM copper industry chain database

>According to market news, there were rumors last week that the US would release a mid-term report on copper tariff issues. With the expectation of an early resolution of tariffs, the LME forward curve structure corrected, with the price spread between November and December dates returning to Flat Backwardation. In the short term, the market's expectations for the balance in H2 have relaxed. This article assumes that the US will finalize tariffs in July and discusses the changes in copper cathode balance and structure in H2 2025 after the tariffs are finalized.

Supply side, copper concentrates will remain in a relatively tight supply situation in the short term. Following production cuts at Kamoa-Kakula due to an accident, miners have become more aggressive in their expectations for the Benchmark. The spot TC has also shown no signs of recovery. Although Chinese smelters are maintaining relatively high production levels supported by long-term contract ore and raw materials, smelters in Japan, Chile, and other regions have successively implemented production cuts or even shutdowns. The expectation that the tight balance of copper concentrates will transmit to copper cathode in H2 continues to increase, and a new round of capacity replacement cycle is expected to begin for both new and old capacities.

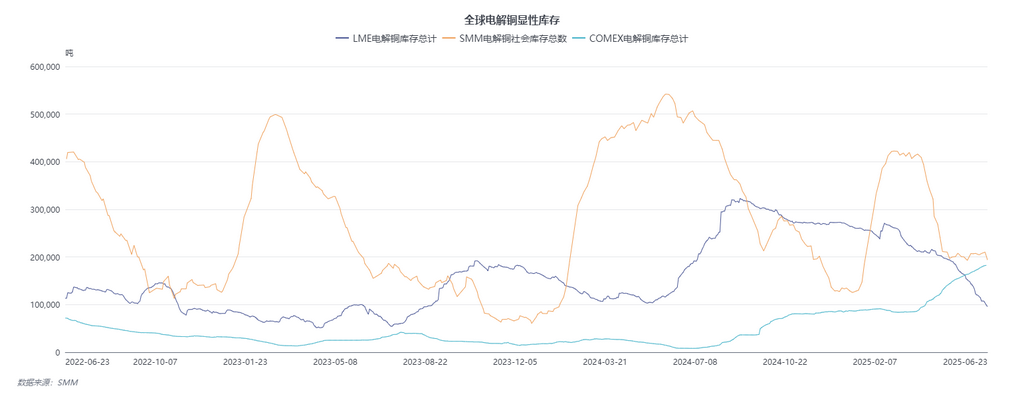

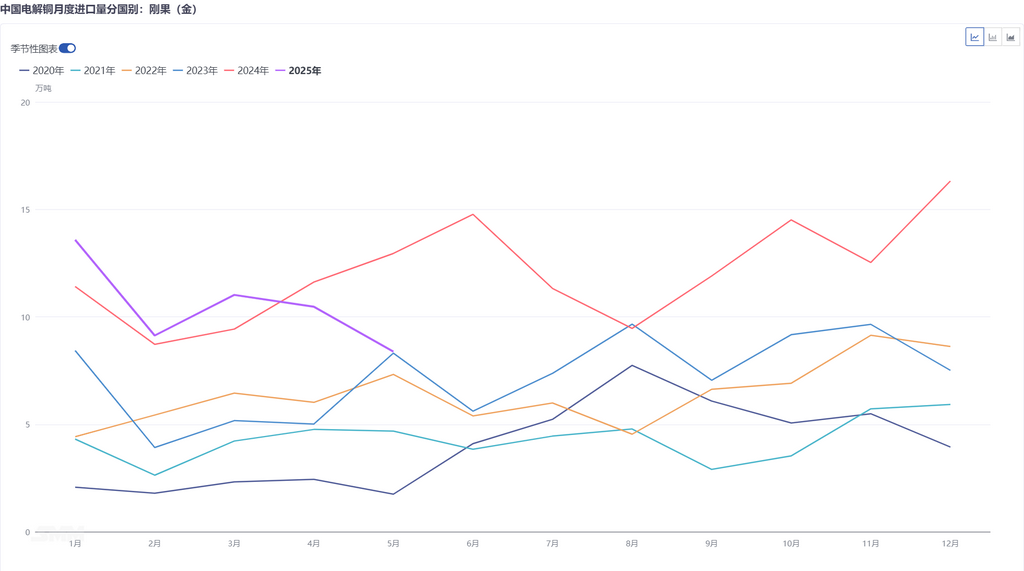

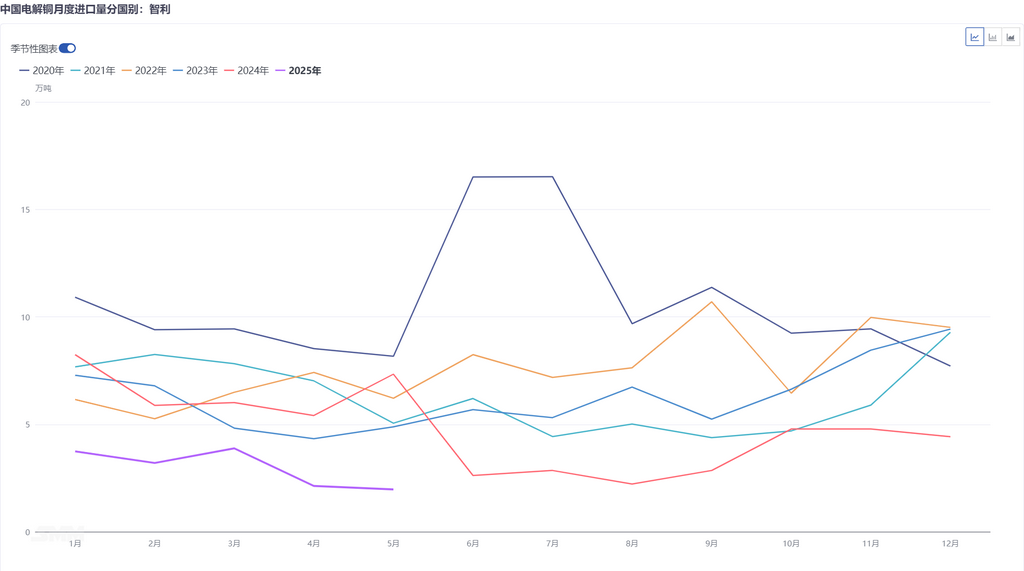

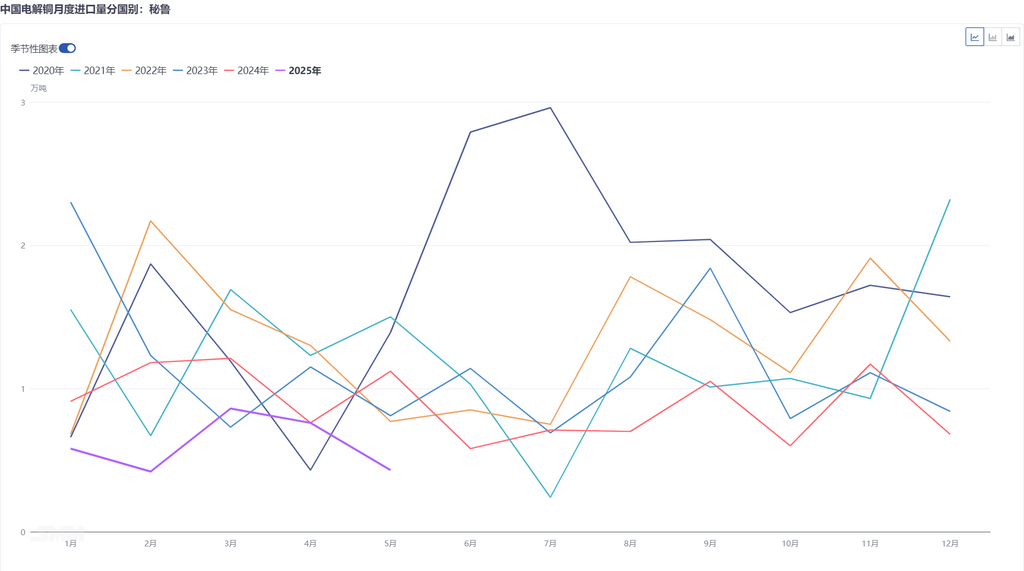

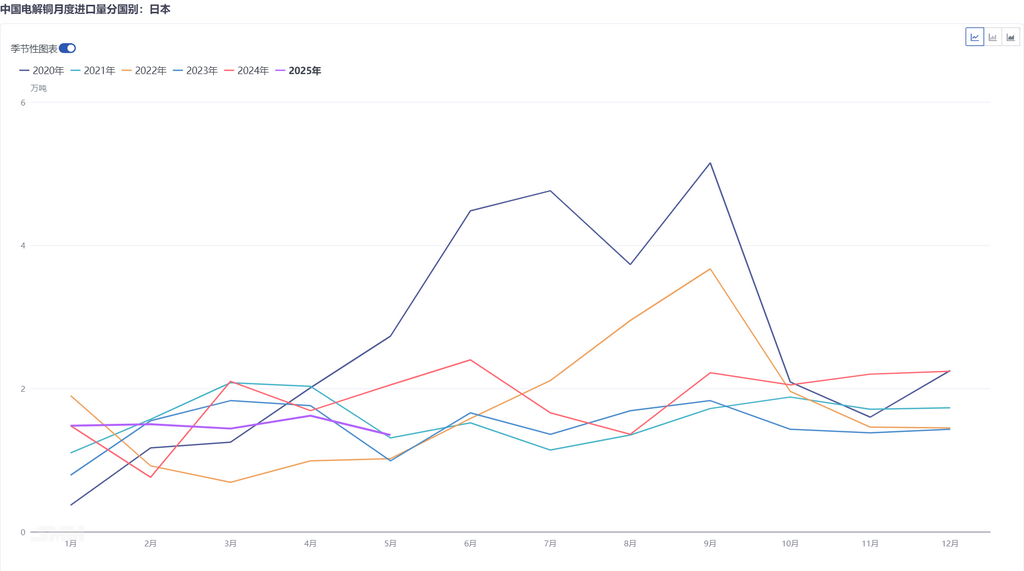

Copper cathode balance side, although there appears to be a surplus in copper cathode supply in 2025, if we exclude the copper cathode inventory siphoned off to the US due to the LME-COMEX price spread, the balance in non-US regions, particularly in the Asia-Pacific region, is actually tight. Currently, both the LME and China's visible inventories have fallen to around 100,000 mt, and supply pressure in Q4 is continuously increasing. From the perspective of global trade flows, Africa still maintains a monthly average of around 20,000 mt of new copper cathode shipments to the US, while South America accounts for the vast majority of US import supply, with shipments to China amounting to less than 25,000 mt per month. European demand has also diverted some of Africa's copper cathode, with Europe importing 90,000 mt of copper cathode from Africa from January to May 2025, up nearly 40,000 mt YoY. The most direct impact is that China's imports of copper cathode from Africa from January to May 2025 were 559,100 mt, a decrease of 3.95% compared to the same period in 2024, and imports from South America were only 180,100 mt, a decrease of 52.81% compared to the same period in 2024. As a result, LME Asian copper cathode inventories continue to destock to fill the gap. Meanwhile, due to ongoing maintenance and production cuts at smelters in Japan and South Korea, the demand gap for copper cathode in Southeast Asia has increased, attracting some domestic copper cathode outflows.

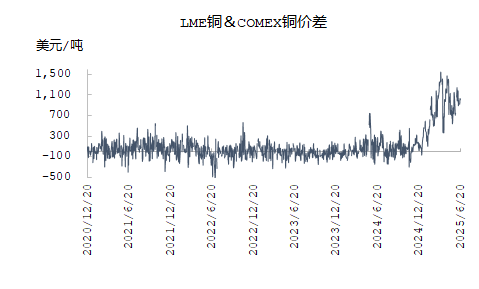

Assuming that US tariffs are finalized early in July, the spot market should maintain the following unchanged: 1. The tight supply of copper concentrates will accelerate the replacement of old and new capacities in the Asia-Pacific region, leading to a tighter copper cathode balance in Asia in the short term. 2. The LME-COMEX arbitrage will persist from June to July. Copper cathode shipments in transit but not yet delivered to COMEX warehouses may be redirected to LME warehouses in New Orleans after tariff implementation, temporarily flattening the backwardation structure in LME far-month contracts. 3. In Q4, domestic smelters may face intensified losses due to deteriorating long-term contract figures, potentially leading to voluntary production cuts before 2025 contract negotiations. If the US copper tariff investigation concludes early in July, two impacts may emerge: 1. The LME-COMEX price spread will narrow, with the far-month backwardation structure contracting short-term. African and South American copper cathode supply will improve after August, slightly easing Asia's tight balance in Q3. 2. Copper cathode already in the US will remain there due to cost and COMEX structure constraints, with existing inventories continuing to deplete. This will depress US offshore market premiums, narrowing arbitrage opportunities in non-US regions and gradually normalizing spot premiums. Overall, 2025 copper consumption is expected to maintain above-forecast growth, setting a tight balance tone for H2. Sustainable backwardation structures will persist between LME and SHFE.